Tax Planning for Home Seller

They say that nothing is certain except death and taxes. However, since 1997, the obligation of a homeowner to pay taxes upon the sale of his or her home has become certainly less frequent. Prior to Congress passing the Taxpayer Relief Act of 1997, unless you were older than 55 years of age or bought a more expensive home within two years of selling, you would have had to pay a tax on any profit (capital gain) made on your sale. A capital gain is the difference between the sales price of the home less the sum of the purchase price you paid and the cost of any capital improvements you made. A capital improvement, discussed in detail below, is an improvement made to the home or property which increases its value and/or prolongs its life.

As a result of the Taxpayer Relief Act of 1997, home sellers can breathe a little more easily. Now, the law exempts from taxes any capital gain up to $500,000 for married couples filing jointly and up to $250,000 for single sellers. In order to qualify for the exemption, you are required to have lived in the home as your principal residence for 2 out of the 5 years prior to the sale. In addition to establishing these exemptions, the 1997 law also reduced the rate that one has to pay on the taxable portion of a capital gain- from 28% to 20%. When the law was first introduced, home-based business owners who took the home-office deduction on their tax returns, would not be able to obtain a capital gain exclusion on that portion of the home designated as a work place. In 2002, the federal government tinkered with this portion of the law, and now, as long as your work place is located within the home itself, and not in an accessory building on your property, you are entitled to the full tax exclusion on any capital gains realized. The government has also adopted an “Unforeseen Circumstances” exception to the “2 years out of the last 5 years” requirement. If you are forced to sell the property before you occupy it for 2 years due to an event that you could not have reasonably anticipated prior to purchasing and occupying the home, you will be allowed to use the exemption. Such circumstances that would allow you to claim “unforeseen circumstances” are: divorce, death of one of the homeowners, health problems which require you to sell to obtain treatment, loss of employment, multiple births from the same pregnancy, and natural or man-made disasters. Voluntary events such as marriage, adoption, and job relocation probably will not qualify.

To appreciate the significant effect of the 1997 Taxpayer Relief Act, let’s consider the following two examples:

Pre-1997: A married couple under age 55 and in the 31% tax bracket sold their home that they have lived in and owned for 5 years for $400,000 (representing a $100,000 profit) and bought another home in another, less-costly town for $375,000. As they did not purchase a home of equal or greater value, they would have had to pay $100,000 (capital gain) x 28%; or $28,000.

Post-1997: Using the same facts, since the couple lived in and owned the home for at least 2 of the last 5 years, and since the capital gain is less than $500,000, this married couple will pay zero capital gains tax.

Even though capital gains tax obligations are now fewer in number as a result of the law change, they nevertheless can still be quite, shall we say, taxing. As a result of the very strong surge in property values over the last decade and in years before, it is common for homeowners who have lived in their home for some time to sell their home for at least $250,000 or $500,000 more than they originally paid. When this is the case, it is important to attempt to minimize tax liability by maximizing your home’s basis. The basis is the value of your investment in the property. It includes the purchase price plus acquisition costs (i.e. closing costs) plus capital improvements.

To calculate your full basis, you (and your tax advisor) will first need to have a complete breakdown of the closing costs you incurred at the time of your purchase. The settlement statement will provide you with these figures. Next, you will need to add up the allowable capital improvements. In order for a home expense to qualify with the IRS as a capital improvement, it must improve the value of your home. Expenses incurred purely for cosmetic or maintenance purposes will not work. An addition to the home, a new kitchen, finishing the basement, or the installation of an in-ground pool are capital improvements; a replacement roof, grass cutting and snow removal expenses, and home heating fuel are not. For a comprehensive list of IRS allowed capital improvements, see IRS Publication 523, available at www.irs.gov. So, for example, if you paid $350,000 for your home, paid $7,500 for closing costs, including mortgage points, bank fees and attorney’s fee, and you paid $25,000 for improvements during your ownership, including the planting of new bushes, a finished basement, and new kitchen cabinets, your basis would be: $382,5000. If you instead inherited your home, your basis is the fair market value of the property as of the date of death of the prior owner.

In addition, in determining tax liability, you are allowed to use the net selling price. Therefore, be sure to add up the many costs you incurred as a result of your sale. These include the somewhat obvious: sales/ stamp tax, broker’s fee, attorney’s fee, recording costs; and the not-so-obvious: costs incurred in sprucing up the home for sale, advertising, and the fee for the lawn sign.

To better understand the current capital gains law, lets apply it to some varying fact patterns:

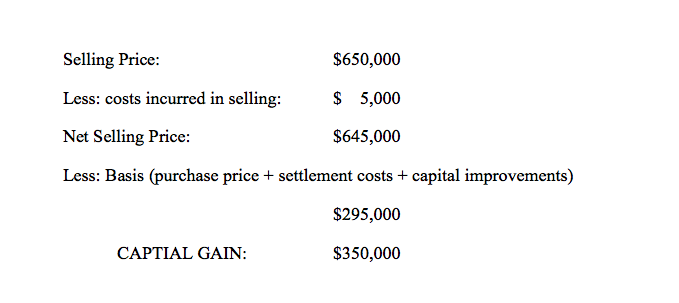

1) Nick and Margaret, a married couple who file jointly, bought their home in 1990 for $250,000 plus $5,000 in closing costs. They lived there as their principal residence continuously until 2005 when they sold it for $650,000, with $5,000 in closing and marketing costs. Over the years, the spent $40,000 for capital improvements. Their capital gain is $350,00:

There is no tax due because they: 1) are married; 2) lived in the property for 2 out of the last 5 years; and 3) the gain is less than the $500,000 exemption.

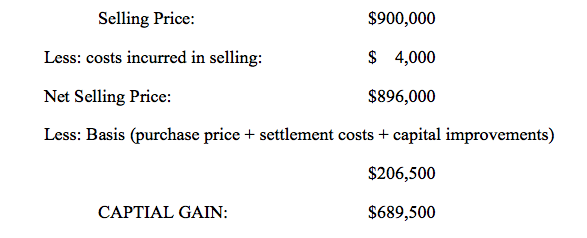

2) Joe and Carol, a married couple who file jointly, bought their home in 1975 for $80,000, plus $1,500 in closing costs. They have lived in it together until 2005 when they sold it for $900,000. They incurred $4,000 in costs to sell their home. They saved receipts and confirmation of expenses over the years showing capital improvements of $125,000. Their capital gain is $689,500.

Because the capital gain is greater than the $500,000 allowable exemption, they have a tax liability. They will have to pay: ($689,500 – $500,000) x 20%; or $37,900.

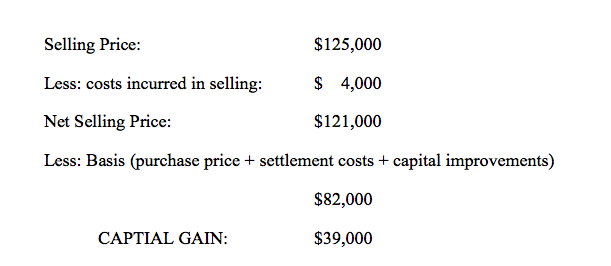

3) Millie bought her condo in 1996 during the buyer’s market and paid $75,000 and paid $2,000 in closing costs . She sold it 20 months later when she was able to get $125,000 for it, after paying $5,000 in capital improvements and $4,000 in closing costs. She has a capital gain of $39,000.

Although Millie’s capital gain is less than the $250,000 exemption, she will be liable for the capital gains tax because she did not live in the house for at least two years and does not qualify for the exemption. Millie will have to pay: $39,000 x 20%; or $7,800.

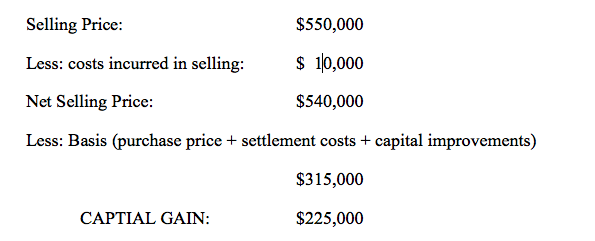

4) Jim bought his house in Connecticut in 2000 for $300,000 and paid $5,000 in closing costs. After he moved in, he finished the basement at a cost of $10,000. The next month, his company transferred him to Texas to work for three years. Believing he would return back to Connecticut, he kept his house and rented it over the next 3 years. The “temporary” position in Texas turned into a permanent opportunity and Jim sold his Connecticut house in 2003 for $550,000, incurring $10,000 in closing and marketing costs. His capital gain is $225,000.

Although Jim’s capital gain is less than the $250,000 exemption, he did not occupy the home as his principal residence for 2 out of the last 5 years; he rented it out. Therefore, he does not qualify for the exemption. Jim will have to pay $225,000 x 20%; or $45,000.

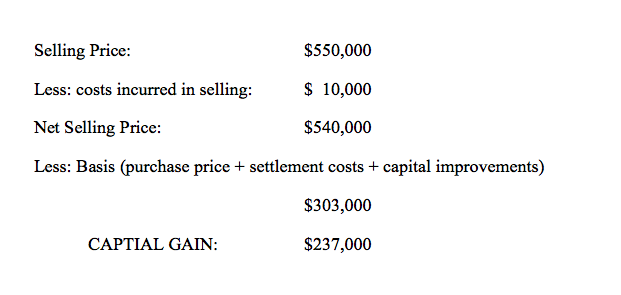

5) Chris and Deb, a married couple filing jointly, bought their house in 2002 for $250,000 and paid $3,000 in closing costs. At that time, Deb started a chocolate truffle business out of her home and wrote off 20% of the home as business use. Chris and Deb spent $50,000 on capital improvements. In 2005, they sold their home for $550,000, after incurring $10,000 for marketing and closing expenses. Their capital gain is $237,000.

As a result of the 2002 alteration to the law, Chris and Deb will be able to use the full $500,000 tax exemption and no capital gains tax will be due. Chris and Deb will be responsible for paying back the depreciation deduction that they have taken over the years at the rate of 25%.

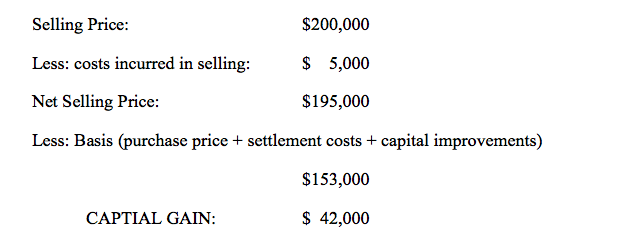

6) Steve and Erica bought their 1 bedroom condo after their wedding in 2002 for $150,000 with $3,000 for settlement costs. The following year, Erica became pregnant and gave birth to triplets. The condo was much too small and they were forced to sell in order to buy a larger home. They sold their condo in 2003 for $200,000 after not incurring any capital improvements. They incurred $5,000 in sale and marketing costs. Their capital gain is $42,000.

While they would normally have to pay a capital gains tax of $8,400 (20% of the $42,000), they sold as a result of unforeseen circumstances; namely the birth of triplets. They will be able to use this exception and avoid any capital gains tax.

If the seller informs the closing agent in writing that there is no chance for any capital gains tax liability, generally, the settlement agent will not file the 1099-S form. The settlement agent will use a form similar to that re-printed below to determine if such reporting is necessary. In order for eliminate the need for reporting, the settlement agent will need to see that all of the form’s questions have been answered “Yes”. (As a result of some double negatives used in the form, it may be easier to read the questions this way- if the statement is true, then check “Yes”. If not true, “No” should be checked.)

1031 Exchanges

While those who are selling investment property are not entitled to the capital gain exclusion, they may be able to defer paying the tax if they purchase another income property of equal or greater value. This is referred to as a “Like-Kind Exchange” or a “1031 Exchange” after section 1031 of the Internal Revenue Code that states that no gain (or loss) shall be recognized on an exchange of property held for productive use for a business or for investment. In order to take advantage of this provision, the property seller must retain the services of a qualified section 1031 intermediary company prior to selling the property. As the sale proceeds are not allowed to be in the seller’s possession, the intermediary will hold the proceeds until a new “replacement” property is identified for purchase. The seller is required to identify the replacement property within 45 days of selling the “relinquished” property. In addition, the seller must purchase the replacement property within the “exchange period” which ends within the earlier of 180 days after selling the relinquished property or the due date for the seller’s tax return.

In order to qualify for a full tax deferral, the seller must meet two requirements. First, he or she must reinvest all proceeds into the replacement property. Second, he or she must acquire the replacement property with an equal or greater amount of debt. If the seller fails to do either of these, the I.R.S, considers any applicable amount to be a benefit to the seller, and he or she will be liable for a tax.

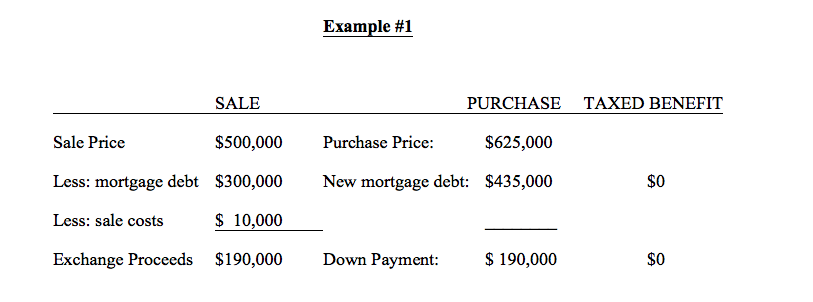

Here, the Seller obtained the replacement property using all of his $190,000 sale proceeds and obtained a mortgage greater than what he previously had. Therefore, he will be able to defer all of the capital gain taxes.

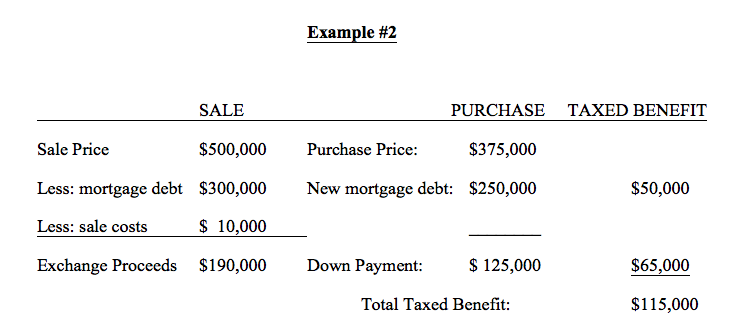

Here, the Seller incurred less debt and used less than his full sale proceeds. Consequently, the IRS will determine that he obtained a $115,000 benefit, and this will be taxable.